In today’s fast-paced economy, simplifying taxation is essential for fostering business growth and ensuring transparency. The GST are having in all assets having now days. Just like Goods and Services Tax (GST) is a transformative indirect tax system designed to unify multiple taxes under a single umbrella. The taxpayers are paying taxes to the government on everything that is made by the government for us. These taxes are made by the government, for the nation. Implemented in many countries, including India in 2017, GST replaced a complex web of central and state taxes, creating a seamless process for the movement of goods and services.

The information about the text is made by the Indian government, and if any kind of changes happen in it, it will be informed by the people who are working there. The statement on which GST is going on in one nation, one tax. Those who are paying the tax are the right people because they are helping the government for the national improvement in our country.

It is structured into various slabs to accommodate different types of goods and services, ensuring fairness while encouraging economic efficiency. Beyond its fiscal benefits. The benefits that are coming towards us are because of us and for us. The changes that come are good for us with these texts. It creates a continuity of working or developing in our country and improves our resources.

The taxes are very high these days, which needs to be stable, and some prices need to be low. The GST strengthens compliance, reduces tax evasion, and brings clarity to consumers and businesses alike. Taxes are necessary to pay to the government. This is the first rule here. These days the tolt ex are not very far apart from each other. Also In this essence, GST is not just a tax reform; it is a step toward modernising the economy, promoting transparency, and fostering inclusive growth for all stakeholders.

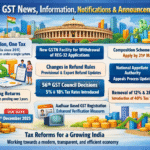

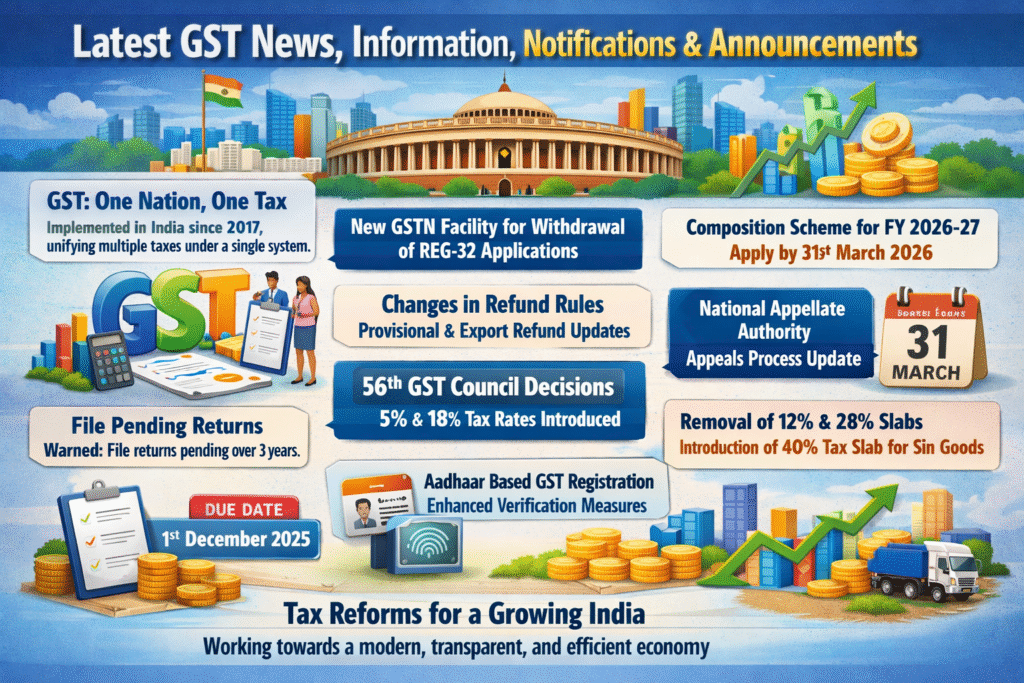

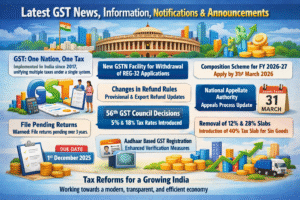

Did you know that the GSTN has introduced a new facility on the GST portal for taxpayers to withdraw their application opting into the 3-day GST registration grant, in form REG-32. Lots of more things about the new withdrawal facility under CGST Rule 14A. which everyone needs to understand first. Before taking any decision.

Regular taxpayers wishing to use the Composition Scheme for FY 2026-27 must do so by 31st March 2026. Likewise, exporters planning to submit a Letter of Undertaking (LUT) for GST-free exports in FY 2026-27 should complete this by the same date. Additionally, the “Additional Notices & Orders” section has been consolidated into the existing “Notices and Orders” tab for easier access and streamlined navigation.

The taxes are also never be the same; sometimes they increase, or some time it goes down. You can see nowadays that the tax is on everything, or even on anything you want. You can also notice the switching of the rate of the text. Not only the single tax we are paying, but along with it, we are paying on small items too.

In this, there are firstly the budget is decided then anything goes forward after that. The balance sheet will be prepared, and then the working and any kind of changing happening after this. In the place of supply for intermediary services as per section 13 of the IGST Act, the special rule for intermediary services is being removed. Some rules can be deduced so that people can easily pay the taxes.

Here, if we are talking about the refunds, we know that the provisional refunds extended to the inverted duty structure (Section 54(6) of the CGST Act): Taxpayers claiming refunds due to the inverted duty structure will now be eligible for provisional refunds. So, the government need to give back its money. They are refunding on a reasonable basis.

If we are talking about the export refunds (Section 54(14) of the CGST Act), we find that the minimum refund limit no longer applies to exports where tax has been paid. The taxes are refundable, but very few and only with strong reasons. The taxes are generated for the ongoing export and import system, too. Not only are these texts also being on the exports and imports system too. These taxes are putting every where in the world where the import and export system is going on.

The orders from the government state that until the National Appellate Authority is set up, the Central Government can empower an existing authority or tribunal to hear appeals under Section 101B. As per the advisory dated 29th December 2025, the GST portal will soon implement hard validations instead of just warnings for negative balance in ECRS and RCM liability ledgers, as well as any excess ITC reclaims.

Any adviser cannot proceed to filing there GSTR’s, and on the electronic materials, they reclaimed statements and ITC reserved in claims. The locals are paying the taxes, and they continue because the offices and jobs are coming under the sector from where the taxes are generated. In 2025, the GSTN issued a new advisory for Invoice Management System (IMS) users.

Only the government authority is having right to make tax-free things or higher means increasing the tax rate of tax on some things or lowering the tax on some things. All the information’s are comes from the head offices of the government.

Accordingly, the Bill of Entry (BoE) filed by the taxpayer for the import of goods, including imports from SEZ, is now available in the IMS. Taxpayers can take suitable action on individual BoE from the October 2025 period onwards. We also heard that, GSTN Advisory Taxpayers are urged to file any pending GST returns that were due three years ago or earlier and remain unfiled up to the November tax period.

Their taxes are changing after their fixed time duration, which they have on a particular text. If you have any pending deals with the government payment, you are also going to get a penalty for that if you have any dues on taxes.

Accordingly, returns of the period October 2022, which are monthly returns, in the July-Sept 2022 quarter (GSTR-1/3B Quarterly), also here FY 2021-22 (GSTR-4), and FY 2020-21 (GSTR-9/9C) will not be allowed for filing from 1st December 2025. Some rules are never changed, and they will be followed strictly.

One common thing that we all know is that GSTN’s advisory is to file pending returns before the expiry of three years. Which were returns (month/quarter ending September 2022) will be barred for filing after the expiry of three years. Some taxes are filed at the end of the month end and some are filed in the middle of the month and monthly.

In this, the upward amendment of the credit note should also be included. The downward amendment of CN, where the original CN was rejected, and the downward amendment of Invoice / DN only where the original Invoice was already accepted. The GSTR-3B has been filed, and ECO-Document downward amendment only where the original was accepted, and GSTR-3B has been filed.

By this study, we know that clearly, where the recipient has not availed Input Tax Credit (ITC) in respect of the relevant invoice or document and which is including no ITC reversal, shall be warranted. The recommendations made at the 56th GST Council meeting were notified by the CBIC on 17th September 2025.

The 56th GST Council Meeting happened on 3rd September 2025 in New Delhi. The government made significant decisions in line with the government’s vision for implementing next-gen GST reforms – GST Council has approved the two-tier GST rate structure of 5% and 18%, removing the 12% and 28% slabs. The GST will be reformed. Also, time to time, it will increase and decrease; the decision is in the government’s hands.

Some changes are occurring in this GST, which are clearly refused. These changes allow claim refunds irrespective of the Demand ID status, but only where the demand amount is negative. In some situation the GST are applied with the conditions applied to it. Some want refunds.

Such persons can claim refunds where the minor head can have a negative balance, even if the cumulative balance is positive or zero, with this some more on which the GST is refused. They also have some negative balance that auto-populates into the RFD-01 refund application.

announced by the GST Council on 23rd August 2025 in New Delhi on the 56th GST Council Meeting, the GST portal automatically suggests the most recent demand order related to a negative balance, being an order-in-original, rectification order or appellate order, etc., for this, the meeting was set. This shows the GST portal automatically suggests the most recent demand order.

These demands are somewhat like this, a negative balance, being an order-in-original, rectification order or appellate order, etc., like this on 23 August 2025, on 3rd and 4th September 2025, in New Delhi 56th GST Council Meeting is set to happen. A rate rationalisation measures are expected here. The government has extended the GSTR-3B due date for July 2025 from 20th August to 27th August 2025.

The CGST notification 12/2025 was issued on 20th August 2025 in this regard. Then, after that, PM Narendra Modi called. The tax structure is proposed to be streamlined by removing the 12% and 28% slabs, with items being reclassified into the 5% and 18% slabs, alongside the introduction of a 40% tax slab specifically for sin goods.

The removal of 12% and 28% tax slabs, while merging items into the 5% or 18% tax slabs. Introduction of 40% tax slab for sin goods.

GSTN issued a communication via its official social media handle regarding the B2C section in Table 12 of GSTR-1. It was observed that taxpayers dealing exclusively in B2C supplies were encountering difficulties when leaving Table 12A (B2B HSN Summary) blank. The department has clarified that even in the absence of B2B supplies, taxpayers are required to include at least one entry in Table 12A. The growing India is now at its peak.

Like so many other GSTs, are being applied by the government. This is very helpful for this country. There are too many decisions taken by the government. These too many GSTs are a complication for this country. so that our country grows and develops differently. Here, the 55th GST Council meeting happened on 21st December 2024 in Jaisalmer, Rajasthan and MFA/2FA will be mandatory on the NIC portal/s to generate e-invoices and e-way bills for taxpayers with an annual aggregate turnover (AATO) more than ₹20 Crores, expanding to all users from 1 April 2025 in a phased manner.

GSTN has been issuing advisories on Biometric-Based Aadhaar Authentication and Document Verification for GST Registration for different states. Some have rules and regulations. Here, Rule 8 now includes Biometric-based Aadhaar Authentication based on data analysis and risk parameters and document verification.

This aims to streamline and enhance the registration process in Madhya Pradesh, Chhattisgarh, Goa, Mizoram, Haryana, Manipur, Meghalaya, and Tripura, which are the states where the above advisory stands applicable. The total credit available for inward supplies in Table 8A will now be auto-populated from GSTR-2B, while Table 8C must be filled manually for credits received during the FY but availed in the next FY. GSTN issued an advisory regarding the mandatory sequential filing of GSTR-7 returns, effective from November 1, 2024. On 1st November 2024, the Government officially released the GST collection report for October 2024 on the GST Portal.

Like these, many more are pending and have different issues and different deals. The GSTs are making their charges on each and every thing. On different dates and their time period. information

More Stories

Top 5 Current Affairs in India in March 2026: Latest News, Key Events & Exam Updates

Silver Rate Today, March 24, 2026: White metal extends losses on MCX, falls over Rs 7500; Check city-wise rates in Delhi, Mumbai, Chennai

World Current Affairs This Week: 22-Nation Coalition Over Strait of Hormuz, Antibiotic-Resistant Cave Bacteria, and US-Iran Oil Sanctions Relief